Energy consumption has become a key focus area for sustainability initiatives, especially with new legislation such as RED III and ESRS setting increasingly higher goals for renewable energy. Companies are striving to step up their corporate sustainability reporting to demonstrate their commitment to sustainability transparently. Energy Attribute Certificates (EACs) play a critical role by enabling companies to claim the environmental benefits of renewable energy and demonstrate their support for a low-carbon future.

In the new version of our ebook, we revisit corporate disclosure and reporting – updated with key information from the latest legislation.

Here’s what you can expect to learn from the ebook:

- The benefits of EACs for corporate disclosure – how do Energy Attribute Certificates incorporate into reporting, and what’s the difference between voluntary and compliance disclosure

- The advantages of using EACs for corporate sustainability reporting

- Using EACs for your sustainability reporting – across organizational departments

- Best practices for corporate disclosure

- How the new legislation may affect your reporting – which organization types and sizes need to start reporting, when, and how

In this blog post, we will summarize those points, but for the full guide, we suggest reading the ebook.

What is corporate disclosure?

Corporate disclosure is the systematic dissemination of information about a company’s financial, environmental, and social performance to its stakeholders. This crucial practice can take various forms, including financial reporting, governance reporting, and CSR reporting, and can be either mandatory or voluntary. Beyond regulatory compliance, corporate sustainability reporting can be valuable for various stakeholders, such as corporate customers looking to partner with ESG-compliant vendors and suppliers, or attracting talent.

The benefits of using EACs for corporate sustainability reporting

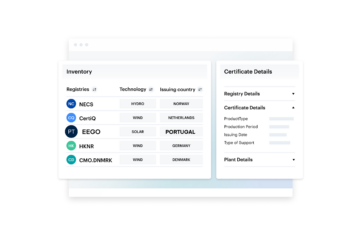

EACs allow organizations to disclose their energy use more easily and efficiently, enabling them to participate in initiatives such as compliance markets, mandatory schemes that require companies to disclose certain information, such as carbon emissions, and voluntary markets, programs in which companies choose to participate voluntarily and opt in to cutting out carbon emission, for example.

Use cases

EACs are instrumental in ensuring companies comply with mandatory renewable energy quotas, such as the Full Disclosure requirements in the Netherlands and Austria. There are various use cases and applications for leveraging EACs for sustainability reporting, on top of providing companies with incentives to promote the use of renewable energy. In the ebook we dive into the following ones: improving transparency, enhancing credibility, increasing stakeholder engagement, meeting regulatory requirements, mitigating financial risks, encouraging innovation, attracting and retaining talent.

Effectively using EACs across your organization

To maximize the benefit of using EACs for corporate sustainability reporting, organizations should follow best practices across processes and departments. The key processes where effective use of EACs should be implemented in order to achieve their sustainability goals and improve their environmental impact are procurement, tracking, and reporting.

The new directive’s impact on corporate sustainability reporting

What is dual reporting – and when is it mandatory?

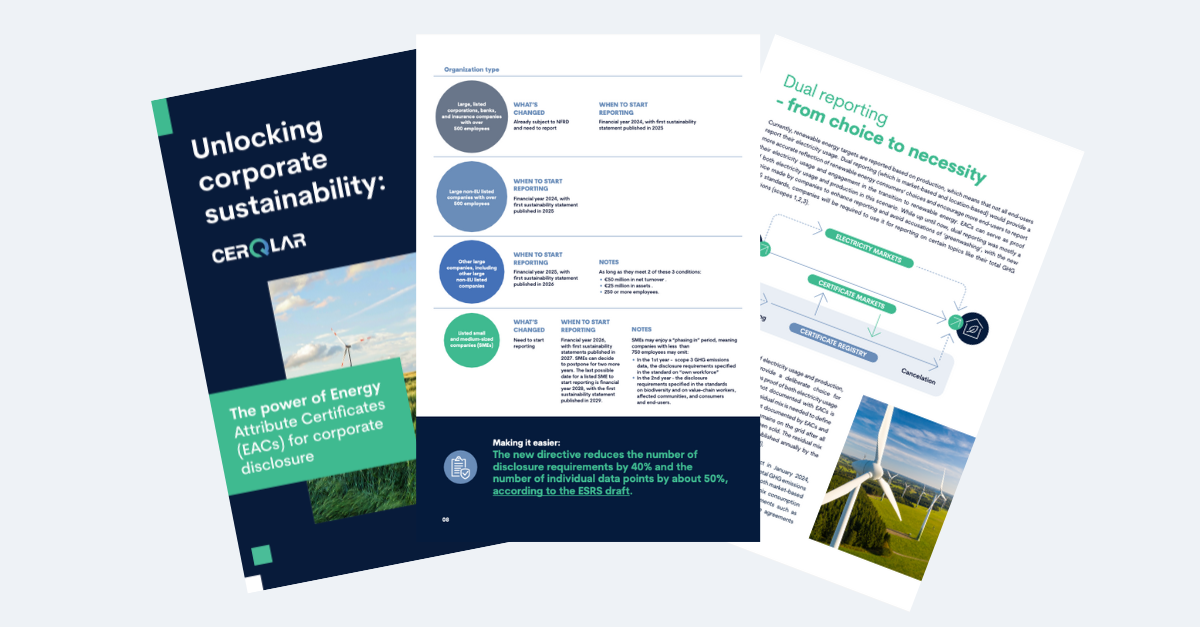

Currently, renewable energy targets are reported based on production, which means that not all end-users report their electricity usage. Dual reporting (which is both market-based and location-based) would provide a more accurate reflection of renewable energy consumers’ choices and encourage more end-users to report their electricity usage and engagement in the transition to renewable energy. EACs are used as “market-based” reporting and can serve as proof of both electricity usage and production in this scenario. While up until now, dual reporting was mostly a choice made by companies to enhance reporting and avoid accusations of ‘greenwashing’, with the new ESRS standards, companies will be required to use it for reporting on certain topics like their total GHG emissions (scopes 1,2,3).

Does your company need to report?

While the new directive reduces the number of disclosure requirements by 40%, it also significantly expands the volume of which organization types and sizes need to report, what the reporting needs to include and when those companies need to start reporting. Most significantly, SMEs (small and medium sized businesses) that are listed in Europe, are now subject to reporting, following the ESRS legislation. The good news is, these companies will only need to start reporting in the financial year of 2026, and may postpone for a couple more years. However, these companies will need to start implementing new habits and processes inside in place very soon in order to be able to create the change management across the organization that will allow them to effectively report when that day comes. To quote Mark Vaessen, KPMG’s Chair of KPMG’s Global Corporate & Sustainability Reporting Topic Team: “Now the final text of the ESRSs is clear, companies in scope have no time to lose before these standards become mandatory. The scale and ambition of these standards is unparalleled and there are key differences to other international frameworks. Companies need to get ready to meet the challenges and realize the opportunities that enhanced reporting will bring.”

Make sure to download the ebook for a detailed table of reporting requirements and timelines.